Uncategorized

This is my archive

Vi har många uppdrag som Taktisk Inköpare och söker nu fler stjärnor som vill bli en del av vårt team.

Det gäller företag i olika branscher och av olika senioritet. Vi lägger inte alltid ut dessa på vår hemsida, utan jobbar främst med aktiv matchning i vår kandidat-bank och i vårt nätverk.

Har du utbildning inom området samt några års erfarenhet från taktiskt inköp, skicka in en spontanansökan idag och få möjlighet till en ny utmaning som en del i ett härligt gäng!

Du erbjuds

Som anställd på SCG kommer du att jobba med spännande uppdrag hos olika kunder inom alla möjliga branscher. Detta gör du som individ eller i team, men oavsett hur det specifika uppdraget ser ut har du alltid ett team av drivna och kompetenta konsulter inom supply chain samt jurister i ryggen. Vi hjälper varandra vid behov för att både utveckla oss som team och individer, samt för att stärka leveransen till våra kunder. Hos oss på SCG får du möjlighet att växla upp både dina kunskaper och din karriär!

Övrig information

Startdatum: Omgående

Omfattning: Heltid

Placeringsort: Västerås

Skicka in din ansökan

Vi går igenom urvalet löpande, så vänta inte med att skicka in din CV. Om du är intresserad och vill veta mer om uppdraget, ta kontakt med Emma;

Emma Söderström

Key Account Manager

Tel: 073 – 026 07 28

Email: emma.soderstrom@scgnordic.se

Om Supply Chain Group

Vi på Supply Chain Group erbjuder konsulter inom Supply Chain Management samt affärsjuridik. Vi går alltid in med ett stort personligt engagemang för att ge en positiv upplevelse i alla relationer med kunder och medarbetare.

Vår vision är

– Att skapa ökad konkurrenskraft, stabilitet och välmående hos våra kunder.

Vår mission är

– Vi lyfter kundens kompetens genom att dela med oss av vår

Vi ser fram emot din ansökan!

Vi frågade ChatGPT, och fick nedan svar.

(Och vi får väl erkänna att vi håller med om…allt.)

En duktig inköpare har ett antal viktiga egenskaper som bidrar till att skapa framgångsrika inköpsprocesser och leverantörsrelationer. Här är några av de främsta egenskaperna:

- Analytisk förmåga: En duktig inköpare behöver kunna analysera data för att fatta informerade beslut om vilka produkter och leverantörer som är bäst för organisationen. Detta innebär att man måste kunna samla in och granska information om leverantörer, produkter, priser och kvalitet, och använda denna information för att välja de bästa alternativen.

- Kommunikationsförmåga: Inköpsprocessen involverar ofta många olika parter, både inom och utanför organisationen. En duktig inköpare behöver ha starka kommunikationsfärdigheter för att kunna förhandla med leverantörer, samarbeta med andra avdelningar och kommunicera inköpsbeslut till ledningen.

- Förhandlingsteknik: Förhandlingar är en central del av inköpsprocessen, och en duktig inköpare behöver ha goda förhandlingstekniker för att kunna förhandla fram bästa möjliga avtal. Detta innebär att man måste vara självsäker, kunna förhandla om priser och villkor, och ha förmågan att nå kompromisser.

- Beslutsförmåga: Inköp innebär att fatta många olika beslut, och en duktig inköpare behöver ha förmågan att fatta snabba och effektiva beslut. Detta innebär att man måste vara analytisk, ha kunskap om marknaden och organisationens behov, och ha förmågan att ta informerade beslut på kort varsel.

- Relationsskapande förmåga: Relationer är viktiga inom alla affärsområden, och inköpsprocessen är inget undantag. En duktig inköpare behöver ha goda relationsskapande färdigheter för att kunna bygga och underhålla långsiktiga relationer med leverantörer, samarbeta med andra avdelningar och skapa förtroende hos ledningen.

- Affärsmässig förståelse: Inköpsprocessen påverkar organisationens bottenlinje, och en duktig inköpare behöver ha god förståelse för organisationens affärsmål och strategier. Detta innebär att man måste ha kunskap om marknaden och konkurrenterna, och förstå hur inköpsbeslut påverkar organisationens resultat och konkurrenskraft.

- Innovativt tänkande: Inköp är en ständigt föränderlig process, och en duktig inköpare behöver ha förmågan att tänka innovativt och hitta nya sätt att förbättra inköpsprocessen. Detta innebär att man måste ha förmågan att identifiera nya teknologier och trender, och använda dem för att skapa mer effektiva och framgångsrika inköpsstrategier.

Aerospace + Defense

•This is a growth segment on the market with demand increasing and a good conversion rate to orders.

Top drivers are FPGAs, MCUs, Mosfets, and Op Amps.

•The fire affecting Vishay Mosfets has had no real impact. There was a slight bump in inquiries, but this did not translate directly into orders.

Prices are stable and lead-times are improving.

Automotive

•Demand is stable but with regional variations. EMEA is still showing strong demand, but it’s down in Japan & North America.

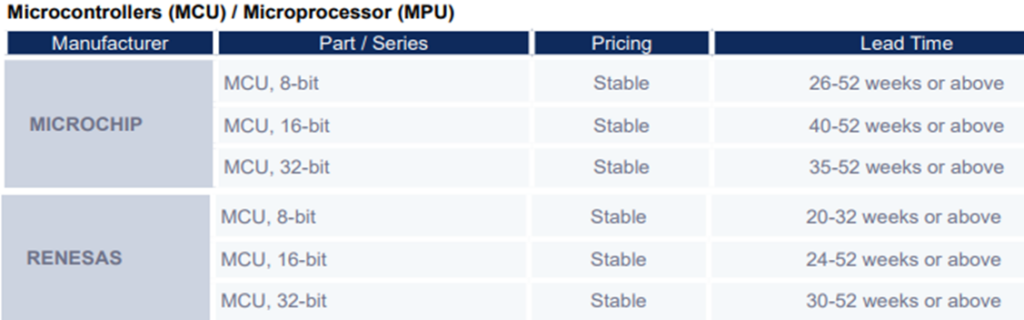

The top drivers are: MCUs, Drivers, Receiver & Transceiver Interfaces, and Mosfets.

•Lead times are improving (except Vishay). Manufacturers have increased pricing so there are not really any PPV opportunities, but we can help with offering security of supply

Health Care

•Overall demand is stable. Top drivers are FPGAs, MCUs & Op Amps. There is more availability in the market with prices still elevated but much lower than a few months ago and more stable than they have been although lead times remain long

Industrial Machinery

•Demand remains stable. FPGAs, MCUs & Op Amps are the top drivers.

•Lead-times remain high with minimum 26 weeks and most still over 50 weeks – however there is more availability in the market.

• Prices are still elevated but much lower than a few months ago.

Modules

•Demand remains stable. Driver, Receiver & Transceiver Interfaces; MCUs; FPGAs & Mosfets are the top drivers.

•There is some improvement on lead-times. The fire affecting Vishay Mosfets has had no real impact. There was a slight bump in inquiries, but this did not translate into orders.

This is a very price sensitive segment.

Consumer Devices

•This is a constant growing segment on the market with demand increasing and a good conversion rate to orders.

•Top drivers are FPGAs and MCUs. Prices are stable and lead-times are improving.

Report by Zoran Boncek – Supply Chain Group

Memory Market:

Shortages for NXP and STM persist into the new year.

•NXP is still struggling to match supply to demand as market availability remains tight for High Voltage MOSFETs and MCU series. Shortages in automotive and industrial parts have shown no signs of easing as these components continue to be among the most constrained. Additionally, demand is rising for the S1912 and MK series, as NXP has maintained hard allocations within certain markets. Q4 allocations are also said to be delayed into 2023.

•Ongoing limited manufacturing capacity is likewise influencing supply of older Freescale series MC9S08, MC9S12, MK and MCF5, all of which have experienced prolonged shortages in the market.

•Similarly, in-demand STM components are not seeing any improvements, a condition which is forecasted to continue for the next six months. STM’s F4, MCU, SPC series and, most notably, automotive parts, have the largest supply and demand imbalance. Supply of STM32 is also particularly unstable within the current market. Lead times and stock availability are under heavy allocation, especially for the F4 series.

Price increases are coming for Xilinx and Silicon Labs’ products

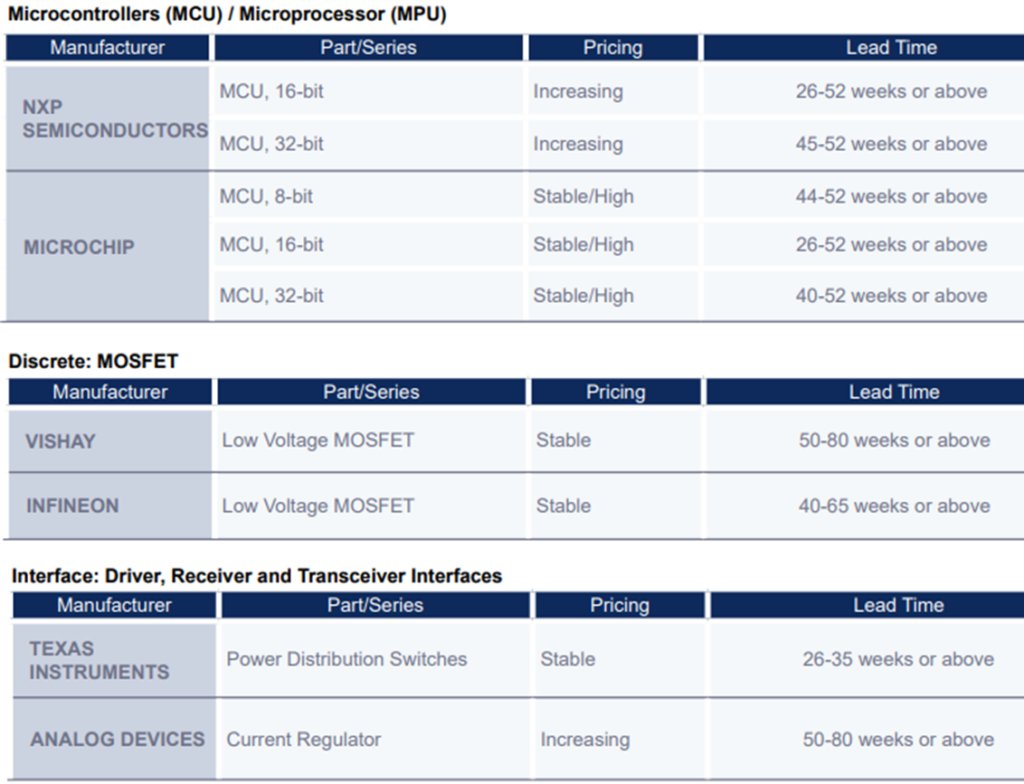

A price increase is reportedly planned across all Xilinx products for the new year. AMD hopes to clear all their Xilinx inventories in 2023 and shorten the lead time cycles for production. Currently, lead times are as follows:

Silicon Labs has also announced its own set of price increases. The official notice sent to customers explained that the price surge was triggered by the global capacity crisis and general inflation in almost all industries, which have caused supply chain costs to rise.

The change will be applied to all existing product lines and Series1 products, including the existing order backlog, on January 1, 2023. The notice mentioned that the price increase does not include series 1 and 2 SoCs and module products, or SOC Wireless Bluetooth series MPNs that start with EFR32xxx.

There is no official documentation on what the price percentage increase will be, but it is expected to be in the range of 15%.

On another note, the Si-xxx series is seeing increased lead times and shortages following its transfer to Skyworks.

China’s wavering COVID-19 policies disrupt the CPU market

The oversupply situation has continued for the CPU industry, as reports from all regions indicate demand is still low. Over the past few weeks, the markets in China have been heavily affected by the return of pandemic restriction policies.

Projection cancellations, production delays and shipment push-outs continue to be an ongoing issue for many factories throughout the country. Consequently, the open market has seen an overwhelming amount of excess inventory being offered and pricing has dropped across every segment.

With the end of year in sight, and a lack of clarity on what the first half of 2023 will bring for pricing trends, the window of opportunity for cost savings may be narrowing.

In addition, China has changed their policies and removed COVID-19 restrictions. This may drive more business into the PC and server markets.

Slow business and weak year-end demand affects AMD and Intel

Intel production is currently focused on the 12th Gen Alder Lake desktop CPU. However, distributors are not building much buffer inventory due to business being slow and the approach of year’s end.

Even though suppliers are hesitant to pull in additional products from Intel, AMD is still working to increase their competitive edge. Recently, the price for AMD’s latest Ryzen 7000 series was adjusted to better compete with Intel’s upcoming 13th Gen Raptor Lake Desktop CPU.

At this time, the 13th Gen Raptor Lake will only utilize K and KF parts from the market. Common series for i3/i5/i7 are expected to launch in Q1 2023. In addition, distributors are anticipating the 14th Gen Meteor Lake from Intel will be available by Q3 2023.

In accordance with the dip in demand, open marketing pricing for Intel Ethernet chipsets has been on a steady decline for weeks. Vendors are currently willing to take losses to alleviate inventory pressure.

Even with open market pricing falling well below Intel’s direct cost, there has yet to be any recovery in demand from customers since they expect prices will continue their downward trend.

Alternatively, open market ex-stock is running low, especially for Desktop Chipset H510 and Intel Ethernet chipset i211AT. An EOL announcement has already been issued for the chipsets and the last product discontinuance date was April 2022.

Hardware

No relief in sight for the storage or memory market

Overall SSD market revenue for Q3 fell to $5.22B, a 28.7% reduction from the previous quarter. Pricing for enterprise SSDs has steadily continued its downtrend, with further hits coming from customers cancelling projects, and resistance to building more excess inventory.

Samsung series S4510, 240GB and 480 GB are still the most requested models and customers have been actively searching for cost-savings opportunities. However, demand is softening, and vendors are pulling in less stock as they are taking losses on their current inventory.

Due to continuous poor demand for memory modules, manufacturers are changing their strategy. Micron and Hynix have cut DRAM and NAND production to reduce price drops. Meanwhile, Samsung has continued production, but has put a stop to falling prices, despite drops coming every quarter. This move comes despite no upticks in demand.

To protect themselves from the daily fluctuations in pricing, distributors are taking orders on a back-to-back basis.

Trends within the GPU market defy forecasts as demand spikes for RTX 30 series

With the tariff exemption expiring on December 31, vendors and customers are still unsure if an extension will be issued. This has resulted in customers buying additional stock, just in case. Pricing is consequently increasing 4-8% on a weekly basis, particularly for the RTX 3090 blower edition.

Despite the launch of RTX 4080 and 4090, demand for the RTX 30 series continues to heat up. Customers are now looking to the open market to source the RTX 3080 and 3090, primarily due to projects and productions not specing in the newer RTX40 series.

Following the initial launch, RTX 4080 demand dipped significantly, largely due to pricing and performance levels in comparison to RTX 4090. There has been a 5% price cut on the RTX 4090 and 4080 series due to the European currency depreciation and the launch of AMD’s 7900 XTX.

NVIDIA’s RTX 4070Ti will be launching on January 5, 2023. This will provide a more complete product range for the RTX series.

While most products see supply improvements, Mellanox switches remain constrained

Lead times are shrinking for most of Mellanox’s products and availability has improved. This is largely thanks to previous double bookings from customers, resulting in an overflow of stock to the open market.

An exception to this is Mellanox switches, which are facing deepening constraints. Due to the shortage of IC and chip components, plus customers’ under-forecasting, lead times for switches have stretched up to 8-12 months. The most affected series are 7800 and 7890. These series are predicted to go EOL in Q2 2023, so vendors are taking lead time orders now.

Shortages impact industrial power supply and Raspberry Pi stock

Most industrial power supplies have extended lead times by 10-24 months, largely due to a shortage of components and the increasing demand for electric vehicles and automated products. Impacted brands include COSEL, Phoenix Contact, Weidmüller, TDK and PULS. Lead times are unlikely to improve in the short term.

Similarly, supply of Raspberry Pi is unable to meet demand, which has surged over the past two to three years due to the computers’ small size and low cost. Direct manufacturer backlog is as far reaching as one-and-a-half years and is only growing as those orders have yet to be filled. Supply would likely need at least another year to stabilize. Subsequently, open market pricing is at least three to five times more than direct pricing.